Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

How Tax Reform Affects Homeowners

How the new tax reform may affect you as a homeowner

New tax legislation was signed into law at the end of 2017, and it included some significant changes for homeowners. These changes took effect in 2018 and do not influence your 2017 taxes. Here’s a brief overview of this year’s tax changes and how they may affect you*.

The amount of mortgage interest you can deduct has decreased.

Under the old law, taxpayers could deduct the interest they paid on a mortgage of up to $1 million. The new law reduces the mortgage interest deduction from $1 million to $750,000. These changes do not affect mortgages taken out before December 15, 2017.

The home equity loan deduction has changed.

The IRS states that, despite newly-enacted restrictions on home mortgages, taxpayers can often still deduct interest on a home equity loan, home equity line of credit (HELOC) or second mortgage, regardless of how the loan is labeled. The Tax Cuts and Jobs Act of 2017, enacted December 22, suspends from 2018 until 2026 the deduction for interest paid on home equity loans and lines of credit, unless they are used to buy, build or substantially improve the taxpayer’s home that secures the loan.

The property tax deduction is capped at $10,000.

Previously taxpayers could deduct all the state, local and foreign real estate taxes they paid with no cap on the amount. The new law limits the deduction for all state and local taxes – including income, sales, real estate, and personal property taxes – to $10,000.

The casualty loss deduction has been repealed.

Homeowners previously could deduct unreimbursed casualty, disaster and theft losses on their property. That deduction has been repealed, with an exception for losses on property located in a federally declared disaster area.

The capital gains exclusion remains unchanged.

Homeowners can continue to exclude up to $500,000 for joint filers or $250,000 for single filers for capital gains when selling their primary residence as long as they have lived in the home for two of the past five years. An earlier proposal would have increased that requirement to five out of the last eight years and phase out the exclusion for high-income households, but it was struck down. Find out more about 2018 tax reform.

How does tax reform affect your plans for buying or selling a home?

The changes in real estate related taxes may change your strategy. Contact one of our real estate professionals at Windemere Bellevue Commons.

*Please consult your tax advisor if you have any questions about how the new tax reform impacts you

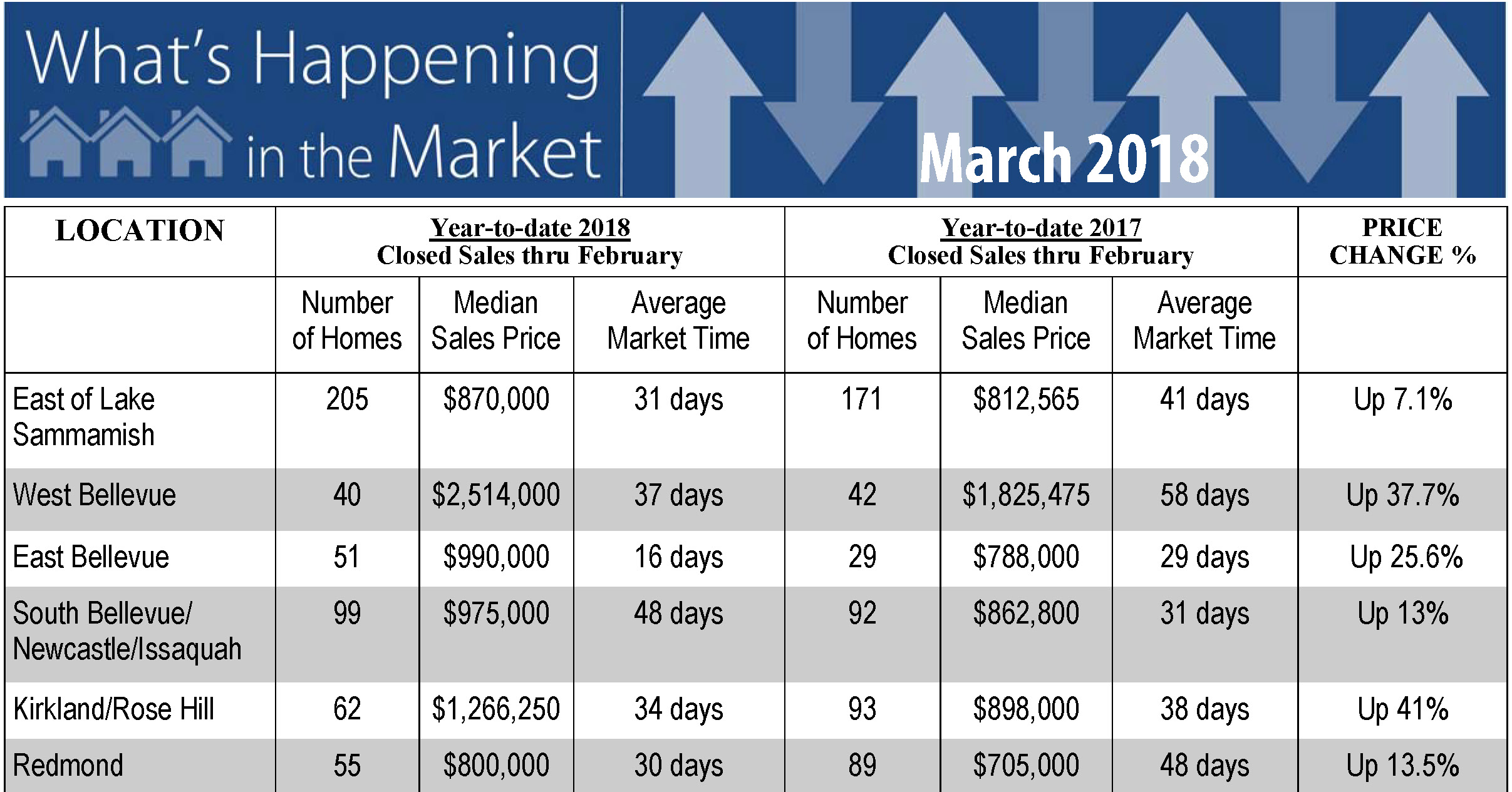

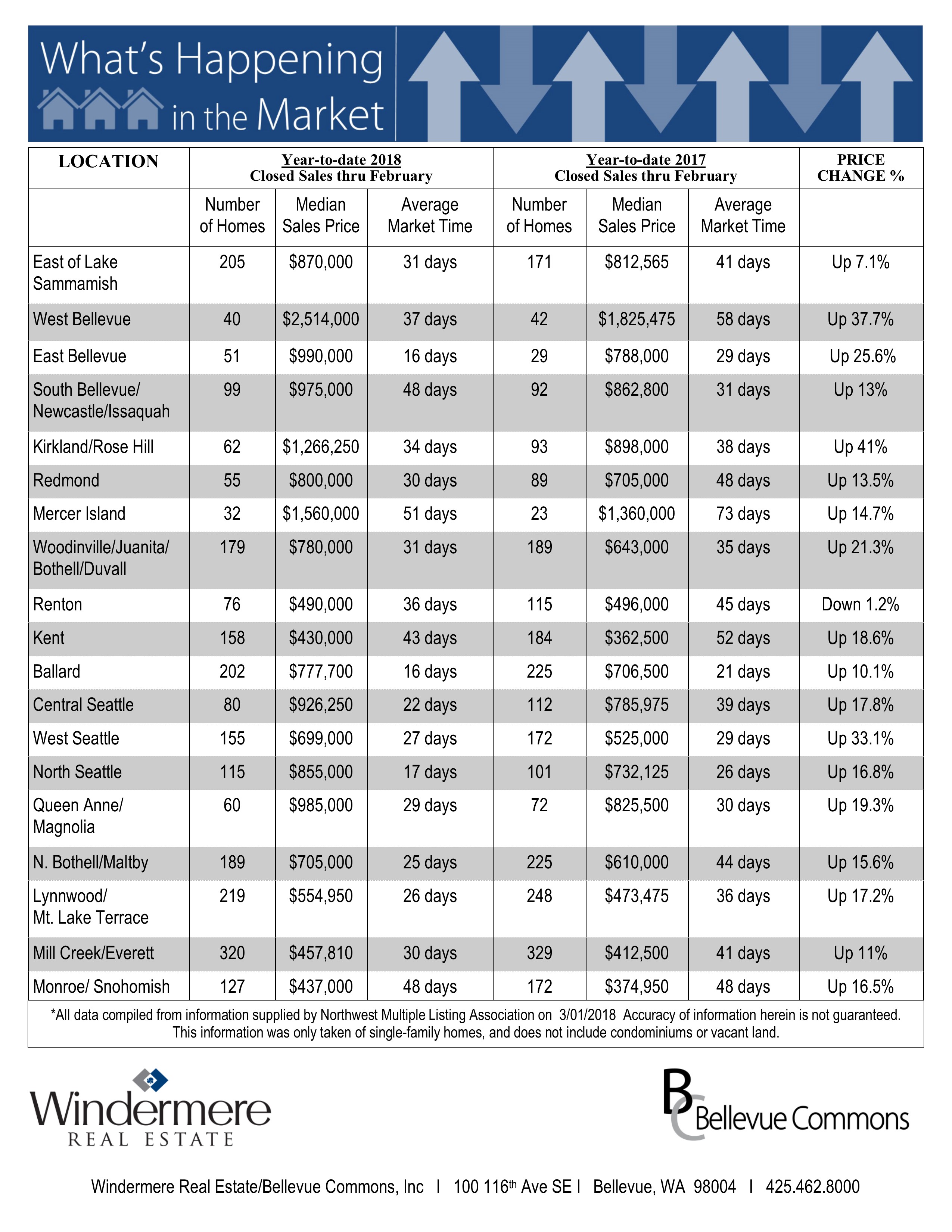

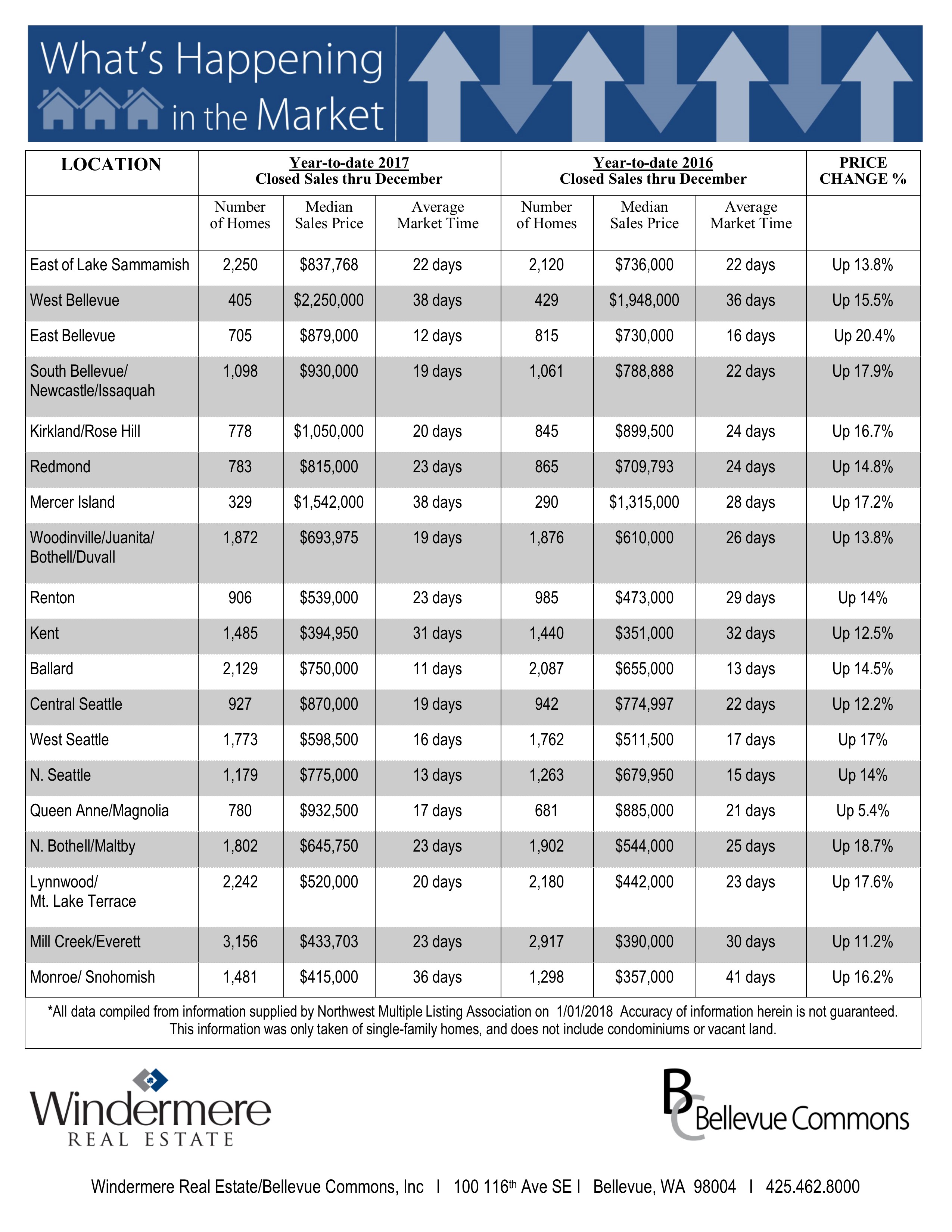

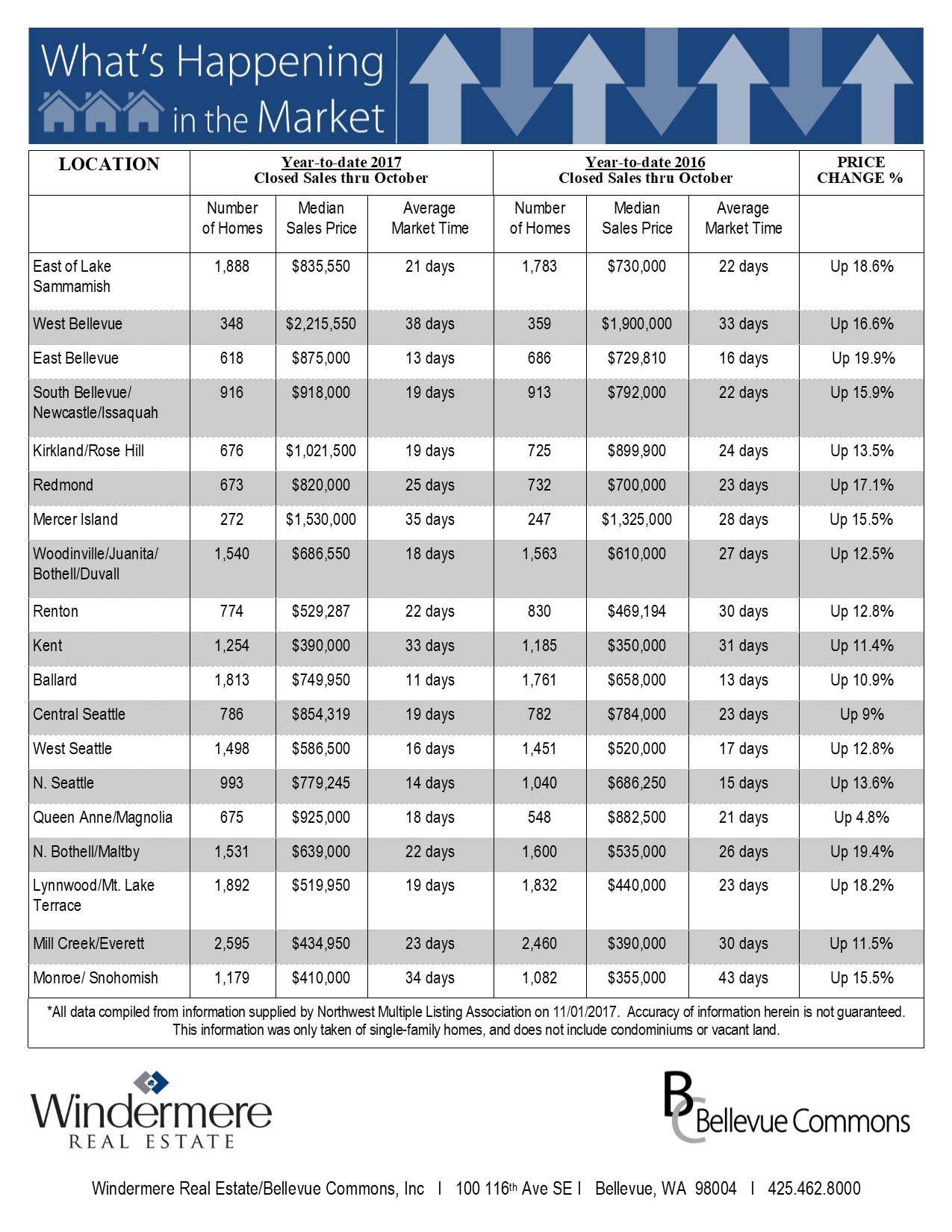

King & Snohomish County Market Stats – February 2018

Median Home prices increased 22% from February 2017 to February 2018

- Active inventory rose 3.3% to 780 properties, but buyers experienced no relief with the median price increasing a staggering 22% from February 2017 to February 2018 ($845,319 from $692,500).

- Over half (52%) of the 529 properties that closed in February sold for over asking price. The median amount above list price was 8%.

- 68% of the closings were on the market for less than 15 days before being Sold!

- Interest rates are a half a point higher at 4.33% than the low of 3.81% in September of 2017.

- We don’t expect to see anything change and if the trend stays the same then we should see the majority of equity gained for 2018 realized over the next 3 months.

Top 5 Reasons to Hire a Real Estate Professional When Buying or Selling!

BUYING OR SELLING A HOME?

See how hiring a Real Estate Professional can benefit you.

Whether you are buying or selling a home it can be quite the adventure, which is why you need an experienced real estate professional to guide you on the path to achieving your ultimate goal. But in this world of instant gratification and internet searches, many sellers think that they can ‘For Sale by Owner’ or ‘FSBO.’

The 5 reasons you NEED a real estate professional in your corner haven’t changed but have rather been strengthened by the projections of higher mortgage interest rates & home prices as the market continues to pick up steam.

1. What do you do with all this paperwork?

Each state has different regulations regarding the contracts required for a successful sale, and these regulations are constantly changing. A true real estate professional is an expert in his or her market and can guide you through the stacks of paperwork necessary to make your dream a reality.

2. Ok, so you found your dream house, now what?

There are over 180 possible steps that need to take place during every successful real estate transaction. Don’t you want someone who has been there before, someone who knows what these actions are, to make sure that you achieve your dream?

3. Are you a good negotiator?

So maybe you’re not convinced that you need an agent to sell your home. After looking at the list of parties that you will need to be prepared to negotiate with, you’ll soon realize the value in selecting a real estate professional. From the buyers (who want the best deals possible), to the home inspection companies, all the way to the appraisers, there are at least 11 different people who you will need to be knowledgeable of, and answer to, during the process.

4. What is the home you’re buying/selling really worth?

It is important for your home to be priced correctly from the start to attract the right buyers and shorten the amount of time that it’s on the market. You need someone who is not emotionally connected to your home to give you the truth as to your home’s value. According to a study by Collateral Analytics, FSBOs achieve prices significantly lower than those from similar properties sold by real estate agents:

“FSBOs tend to sell for lower prices than comparable home sales, and in many cases below the average differential represented by the prevailing commission rate.”

Get the most out of your transaction by hiring a professional.

5. Do you know what’s really going on in the market?

There is so much information out there on the news and on the internet about home sales, prices, and mortgage rates; how do you know what’s going on specifically in your area? Who do you turn to in order to competitively and correctly price your home at the beginning of the selling process? How do you know what to offer on your dream home without paying too much, or offending the seller with a lowball offer?

Dave Ramsey, the financial guru, advises:

“When getting help with money, whether it’s insurance, real estate or investments, you should always look for someone with the heart of a teacher, not the heart of a salesman.”

Hiring an agent who has his or her finger on the pulse of the market will make your buying or selling experience an educated one. You need someone who is going to tell you the truth, not just what they think you want to hear.

Bottom Line

You wouldn’t replace the engine in your car without a trusted mechanic, so why would you make one of the most important financial decisions of your life without hiring a real estate professional?

Source: keepingcurrentmatters.com

The Gardner Report – Fourth Quarter 2017

Western Washington Real Estate Market Update

ECONOMIC OVERVIEW

The Washington State economy added 104,600 new jobs over the past 12 months. This impressive growth rate of 3.1% is well above the national rate of 1.4%. Interestingly, the slowdown we saw through most of the second half of the year reversed in the fall, and we actually saw more robust employment growth.

Growth continues to be broad-based, with expansion in all major job sectors other than aerospace due to a slowdown at Boeing.

With job creation, the state unemployment rate stands at 4.5%, essentially indicating that the state is close to full employment. Additionally, all counties contained within this report show unemployment rates below where they were a year ago.

I expect continued economic expansion in Washington State in 2018; however, we are likely to see a modest slowdown, which is to be expected at this stage in the business cycle.

HOME SALES ACTIVITY

- There were 22,325 home sales during the final quarter of 2017. This is an increase of 3.7% over the same period in 2016.

- Jefferson County saw sales rise the fastest relative to fourth quarter of 2016, with an impressive increase of 22.8%. Six other counties saw double-digit gains in sales. A lack of listings impacted King and Skagit Counties, where sales fell.

- Housing inventory was down by 16.2% when compared to the fourth quarter of 2016, and down by 17.3% from last quarter. This isn’t terribly surprising since we typically see a slowdown as we enter the winter months. Pending home sales rose by 4.1% over the third quarter of 2017, suggesting that closings in the first quarter of 2018 should be robust.

- The takeaway from this data is that listings remain at very low levels and, unfortunately, I don’t expect to see substantial increases in 2018. The region is likely to remain somewhat starved for inventory for the foreseeable future.

HOME PRICES

- Because of low inventory in the fall of 2017, price growth was well above long-term averages across Western Washington. Year-over-year, average prices rose 12% to $466,726.

- Economic vitality in the region is leading to a demand for housing that far exceeds supply. Given the relative lack of newly constructed homes—something that is unlikely to change any time soon—there will continue to be pressure on the resale market. This means home prices will rise at above-average rates in 2018.

- Compared to the same period a year ago, price growth was most pronounced in Lewis County, where home prices were 18.8% higher than a year ago. Eleven additional counties experienced double-digit price growth as well.

- Mortgage rates in the fourth quarter rose very modestly, but remained below the four percent barrier. Although I anticipate rates will rise in 2018, the pace will be modest. My current forecast predicts an average 30-year rate of 4.4% in 2018—still remarkably low when compared to historic averages.

DAYS ON MARKET

- The average number of days it took to sell a home in the fourth quarter dropped by eight days, compared to the same quarter of 2016.

- King County continues to be the tightest market in Western Washington, with homes taking an average of 21 days to sell. Every county in the region saw the length of time it took to sell a home either drop or remain static relative to the same period a year ago.

- Last quarter, it took an average of 50 days to sell a home. This is down from 58 days in the fourth quarter of 2016, but up by 7 days from the third quarter of 2017.

- As mentioned earlier in this report, I expect inventory levels to rise modestly, which should lead to an increase in the average time it takes to sell a house. That said, with homes selling in less than two months on average, the market is nowhere near balanced.

CONCLUSIONS

This speedometer reflects the state of the region’s housing market using housing inventory, price gains, home sales, interest rates, and larger economic factors. For the fourth quarter of 2017, I have left the needle at the same point as third quarter. Price growth remains robust even as sales activity slowed. 2018 is setting itself up to be another very good year for housing.

This speedometer reflects the state of the region’s housing market using housing inventory, price gains, home sales, interest rates, and larger economic factors. For the fourth quarter of 2017, I have left the needle at the same point as third quarter. Price growth remains robust even as sales activity slowed. 2018 is setting itself up to be another very good year for housing.

Matthew Gardner is the Chief Economist for Windermere Real Estate, specializing in residential market analysis, commercial/industrial market analysis, financial analysis, and land use and regional economics. He is the former Principal of Gardner Economics, and has more than 30 years of professional experience both in the U.S. and U.K.

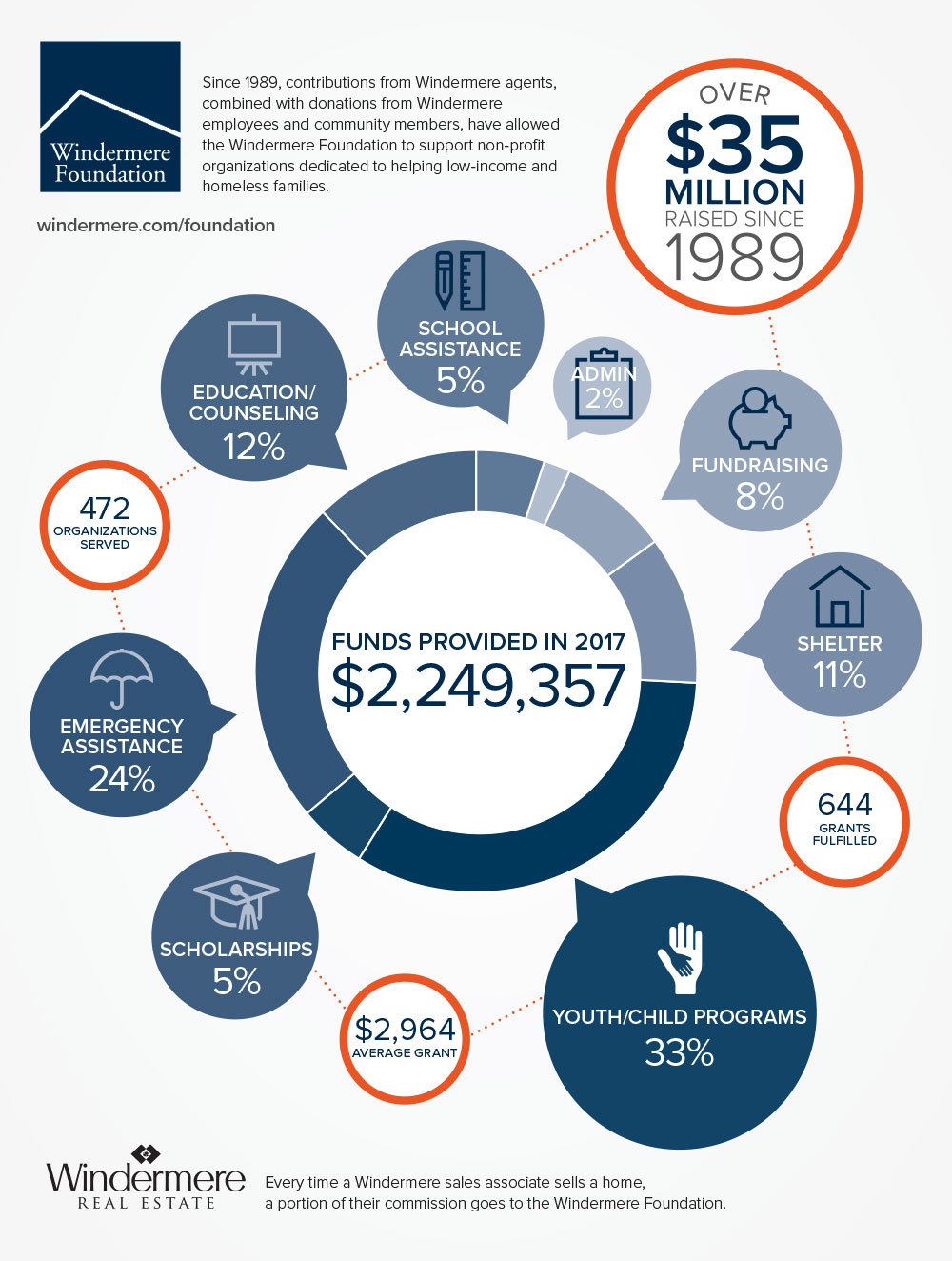

Windermere Foundation Surpasses $35 Million In Giving

Proud to be Windermere…

We are very proud of our brokers to support the Windermere Foundation which has raised over $35 million since 1989. In 2017, Eastside offices alone, raised up to $225,000 to help 22 organizations on the Eastside.

The Windermere Foundation had another banner year in 2017, raising even more than it did the prior year thanks to the continued support of Windermere franchise owners, agents, staff, and the community. Over $2.4 million was raised in 2017, which is an increase of eight percent over the previous year. This brings our total to over $35.5 million raised since the start of the Windermere Foundation in 1989.

A portion of the money raised last year is thanks to our agents who each make a donation to the Windermere Foundation from every commission they earn. Additional donations from Windermere agents, the community, and fundraisers made up 66% of the money collected in 2017. These funds enable our offices to support local non-profits that provide much-needed services to low-income and homeless families in their communities.

SUMMARY OF FUNDS, GRANTS & DONATIONS IN 2017

- Organizations served: 472

- Number of individual grants fulfilled: 644

- Average grant amount: $2,964.04

- Average donation to the Windermere Foundation: $116.08

FUNDING BREAKDOWN

- Total amount disbursed in 2017: $2,249,357.14

- Total disbursed through grants: $1,908,843.54

- Scholarships: 5%

- Youth/Child Programs: 33%

- Emergency Assistance: 24%

- Shelter: 11%

- School Assistance: 5%

- Education/Counseling: 12%

- Administrative Expenses: 2%

- Fundraising Expenses: 8%

So how are Windermere Foundation funds used? Windermere offices decide for themselves how to distribute the money in their local community. Our offices have helped support school lunch and afterschool programs, housing assistance for homeless families, food banks, homeless shelters, and non-profits that provide basic necessities, such as shoes, clothing, toiletries, and blankets to families in need.

A very notable day in 2017 for the Windermere Foundation was November 15, when a record-breaking $253,782 was given in a single day. A total of 35 non-profit organizations benefitted from that day’s donations, including Attain Housing in Kirkland, WA, which received $56,000 from the Windermere Eastside offices. Other organizations that received donations were Boys and Girls Club of Contra Costa in Walnut Creek, CA, and the Shady Cove School in Shady Cove, Oregon.

2017 also marked the second year of our #tacklehomelessness campaign with the Seattle Seahawks, in which Windermere committed to donating $100 for every Seahawks home game defensive tackle to YouthCare, a non-profit organization that provides critical services to homeless youth. While the Seahawks didn’t make it to the playoffs this year, they did help us raise $31,800. When added to last year’s $35,000, that’s a total donation of $66,800. We are grateful for the opportunity to provide additional support to homeless youth thanks to the Seahawks, YouthCare, and the #tacklehomelessness campaign.

2017 also marked the second year of our #tacklehomelessness campaign with the Seattle Seahawks, in which Windermere committed to donating $100 for every Seahawks home game defensive tackle to YouthCare, a non-profit organization that provides critical services to homeless youth. While the Seahawks didn’t make it to the playoffs this year, they did help us raise $31,800. When added to last year’s $35,000, that’s a total donation of $66,800. We are grateful for the opportunity to provide additional support to homeless youth thanks to the Seahawks, YouthCare, and the #tacklehomelessness campaign.

Thanks to our agents and everyone who supports the Windermere Foundation, we are able to continue to make a difference in the lives of many families in our local communities. If you’d like to help support programs in your community, please click the Donate button.

Thanks to our agents and everyone who supports the Windermere Foundation, we are able to continue to make a difference in the lives of many families in our local communities. If you’d like to help support programs in your community, please click the Donate button.

Empty Nesters: Remodel or Sell?

![]()

Your kids have moved out and now you’re living in a big house with way more space than you need. You have two choices – remodel your existing home or move. Here are some things to consider about each option.

Choice No. 1: Remodel your existing home to better fit your current needs.

- Remodeling gives you lots of options, but some choices can reduce the value of your home. You can combine two bedrooms into a master suite or change another bedroom into a spa area. But reducing the number of bedrooms can dramatically decrease the value of your house when you go to sell, making it much less desirable to a typical buyer with a family.

- The ROI on remodeling is generally poor. You should remodel because it’s something that makes your home more appealing for you, not because you want to increase the value of your home. According to a recent study, on average you’ll recoup just 64 percent of a remodeling project’s investment when you go to sell.

- Remodeling is stressful. Living in a construction zone is no fun, and an extensive remodel may mean that you have to move out of your home for a while. Staying on budget is also challenging. Remodels often end up taking much more time and much more money than homeowners expect.

Choice No. 2: Sell your existing home and buy your empty nest dream home.

- You can downsize to a single-level residence and upsize your lifestyle. Many people planning for their later years prefer a home that is all on one level and has less square footage. But downsizing doesn’t mean scrimping. You may be able to funnel the proceeds of the sale of your existing home into a great view or high-end amenities.

- A “lock-and-leave” home offers more freedom. As your time becomes more flexible, you may want to travel more. Or maybe you’d like to spend winters in a sunnier climate. You may want to trade your existing home for the security and low maintenance of condominium living.

- There has never been a better time to sell. Our area is one of the top in the country for sellers to get the greatest return on investment. Real estate is cyclical, so the current boom is bound to moderate at some point. If you’re thinking about selling, take advantage of this strong seller’s market and do it now.

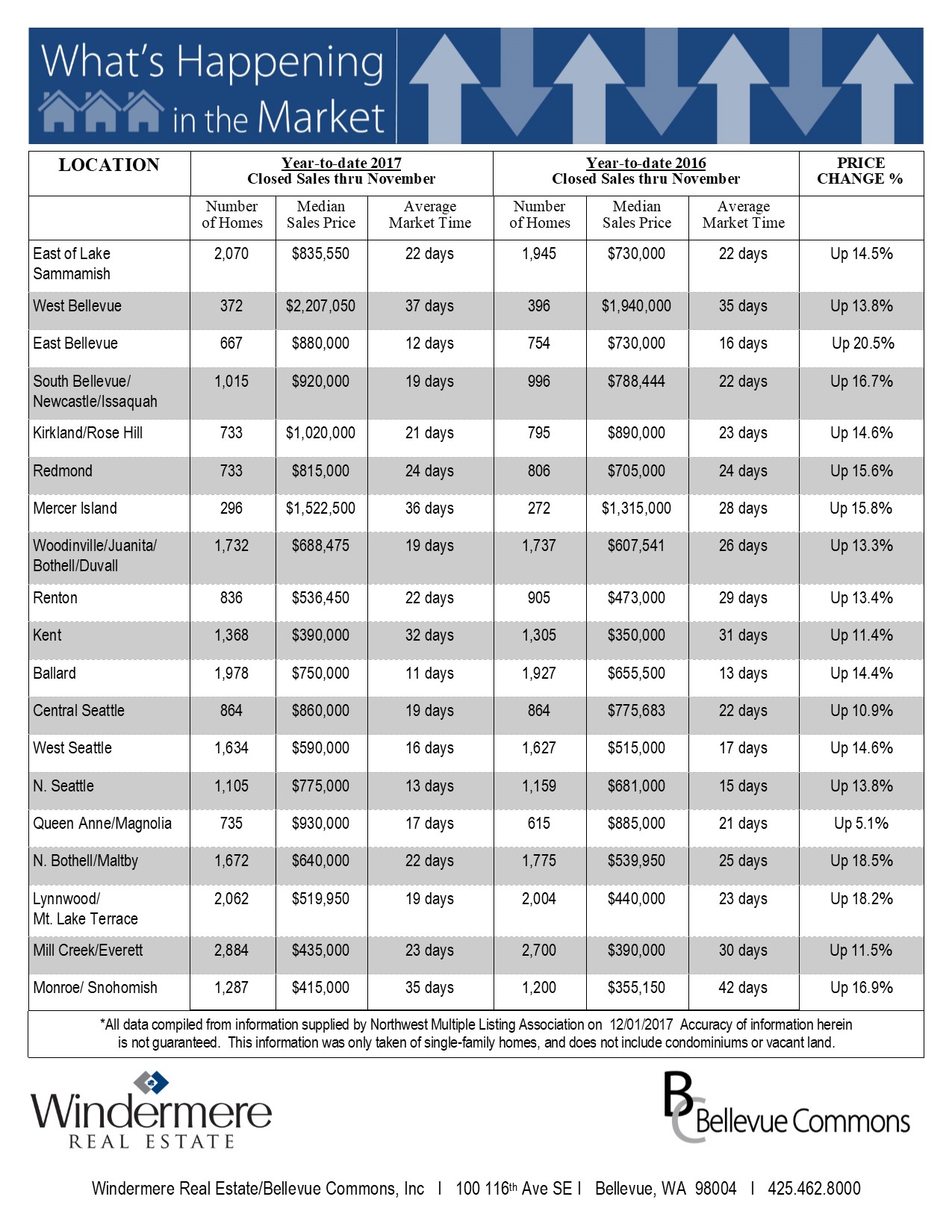

King & Snohomish County Market Stats – December 2017

Home prices nearly double in six years going from $407,000 in December 2011 to $810,000 in December 2017.

The year is over and 2017 has shown to be one of the best years in recent memory for equity gain while creating more and more competition due to dwindling availability of homes. Pricing has recently reached all time highs with the median prices doubling over the past 6 years. That being said we don’t see it changing anytime soon with Consumer and Builder confidence on an all-time high. Those looking to Sell in 2018 will need to position their homes in the best possible light to receive top dollar and Buyers will need to be truly prepared to Buy in order to be awarded a New home in 2018!

Some Highlights

Eastside (based on Residential and Condominium report):

- Home prices nearly double in six years going from $407,000 in December 2011 to $810,000 in December 2017.

- The number of homes sold in December is virtually unchanged from a year ago (538 vs 541) even though there are 22% fewer houses for sale (451 vs 530).

It feels like 2018 will be similar to the past few years. A total frenzy until summer and then a flattening in price for the second half of the year. Interesting consistency in the past three years:

- Big jump in median closed price in December.

- By April or May the closed Median Price has reached the level it will remain close to, until the big jump in December.

King & Snohomish County Market Stats – November 2017

What’s Happening in the Market – November 2017

While the market seems to relaxing for the moment, it appears that the supply is still holding steady below 1 months of inventory. Days on market have been creeping up nominally while the prices seem to have leveled for the moment. This time of year is a nice break from the hectic pace we have been experiencing, but never a better time to list as the competition is at its lowest during the November-December months. Plenty of motivated Buyers out there waiting for homes to become available as there are positive number coming from lenders for Pre-Approvals heading into 2018!

![]()

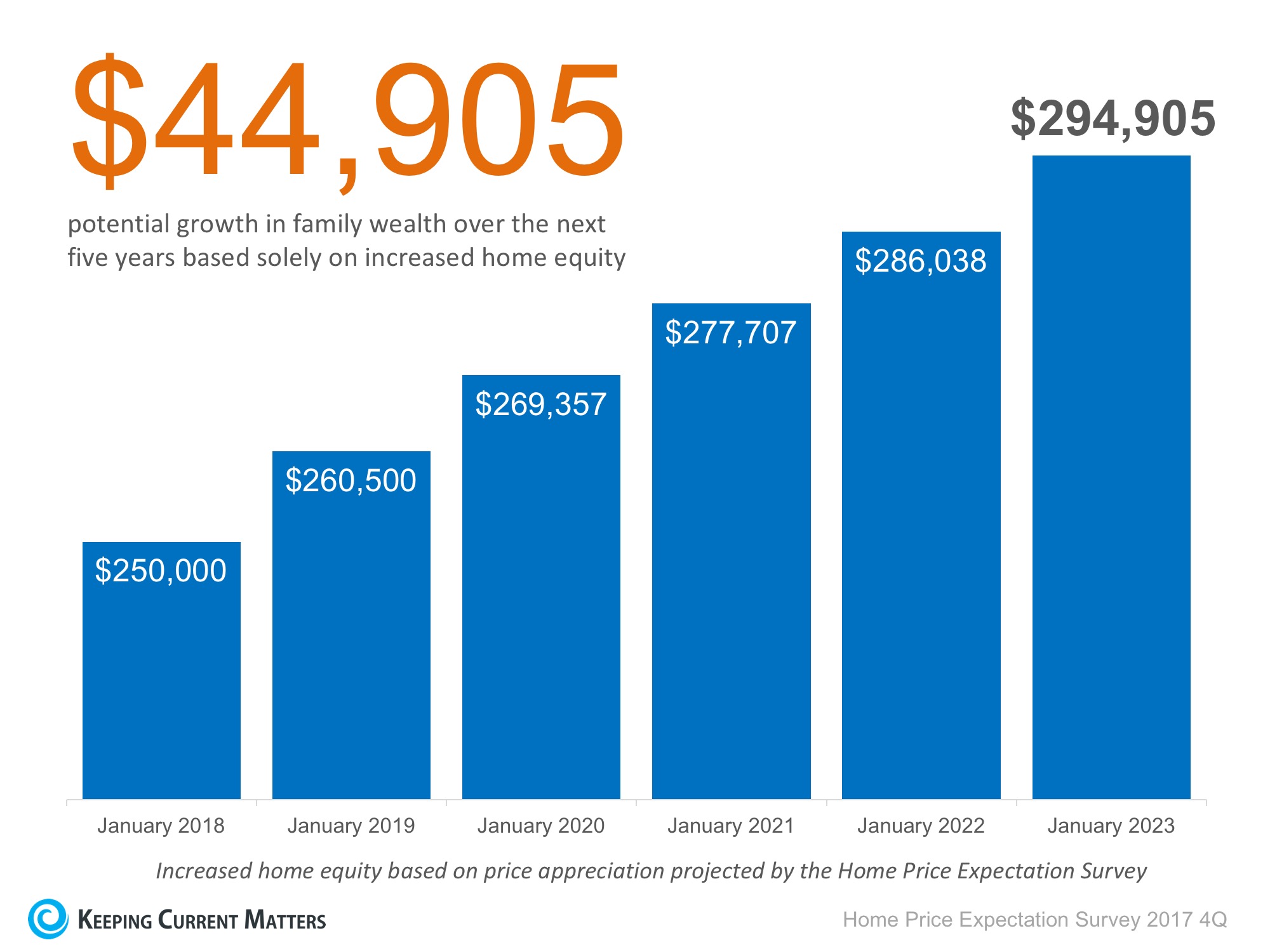

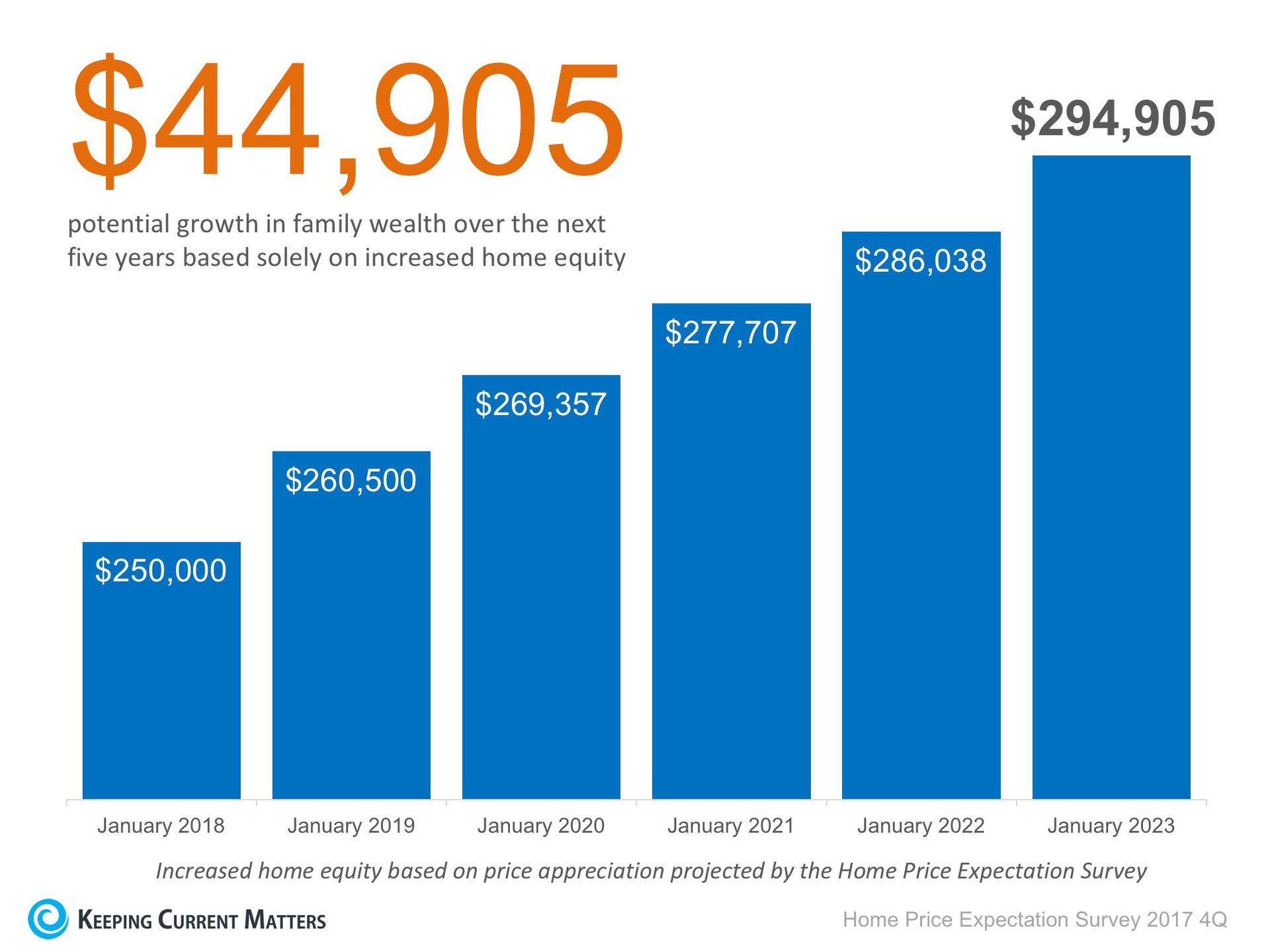

How Rising Prices Will Help You Build Family Wealth In 2018

Homeowners can build wealth by purchasing a home. Over the next five years, home prices are expected to appreciate on average by 3.35% per year and to grow by 24.34% cumulatively, according to Pulsenomics’ most recent Home Price Expectation Survey.

So, what does this mean for homeowners and their equity position?

As an example, let’s assume a young couple purchases and closes on a $250,000 home this month (January). If we only look at the projected increase in the price of that home, how much equity will they earn over the next 5 years?

Since the experts predict that home prices will increase by 4.2% in 2018, the young homeowners will have gained $10,500 in equity in just one year.

Over a five-year period, their equity will increase by nearly $45,000! This figure does not even take into account their monthly principal mortgage payments. In many cases, home equity is one of the largest portions of a family’s overall net worth.

Bottom Line

Not only is homeownership something to be proud of, but it also offers you and your family the ability to build equity you can borrow against in the future. If you are ready and willing to buy, speak to a professional and find out if you are able to today!

Source: keepingcurrentmatters.com

What Can We Expect From The 2018 Housing Market?

2018 Housing Market Forecast

Matthew Gardner, Chief Economist of Windermere Real Estate has recently published a forecast for 2018 housing market. Here are his expectations in 2018.

“It’s the time of the year when I look deep into my crystal ball to see what’s on the horizon for the upcoming year. As we are all aware, 2017 has been a stellar year for housing across the country, but can we expect that to continue in 2018?

Here are my thoughts:

Millennial Home Buyers

Millennial Home Buyers

Last year, I predicted that the big story for 2017 would be millennial home buyers and it appears I was a little too bullish. To date, first-time buyers have made up 34% of all home purchases this year – still below the 40% that is expected in a normalized market. Although they are buying, it is not across all regions of the country, but rather in less expensive markets such as North Dakota, Ohio, and Maryland.

For the coming year, I believe the number of millennial buyers will expand further and be one of the biggest influencers in the U.S. housing market. I also believe that they will begin buying in more expensive markets. That’s because millennials are getting older and further into their careers, enabling them to save more money and raise their credit profiles.

Existing Home Sales

Existing Home Sales

As far as existing home sales are concerned, in 2018 we should expect a reasonable increase of 3.7% – or 5.62 million housing units. In many areas, demand will continue to exceed supply, but a slight increase in inventory will help take some heat off the market. Because of this, home prices are likely to rise but by a more modest 4.4%.

New Home Sales

New home sales in 2018 should rise by around 8% to 655,000 units, with prices increasing by 4.1%. While housing starts – and therefore sales – will rise next year, they will still remain well below the long-term average due to escalating land, labor, materials, and regulatory costs. I do hold out hope that home builders will be able to help meet the high demand we’re expecting from first-time buyers, but in many markets it’s very difficult for them to do so due to rising construction costs.

Interest Rates

Interest rates continue to baffle forecasters. The anticipated rise that many of us have been predicting for several years has yet to materialize. As it stands right now, my forecast for 2018 is for interest rates to rise modestly to an average of 4.4% for a conventional 30-year fixed-rate mortgage – still remarkably low when compared to historic averages.

Tax Reform

Something that has the potential to have a major impact on housing are the current proposals relative to tax reform. As I write this, we know that both the House and Senate propose doubling the standard deduction, and the House plans to lower the mortgage interest deduction from $1,000,000 to $500,000. If passed, the mortgage deduction would no longer have value for home owners who would likely opt to take the standard deduction.

If either of the current proposals is adopted into law, the potential reduction in mortgage-related tax savings means the after-tax cost of home ownership will increase for most home owners. Additionally, both the House and Senate bills also end tax benefits for interest on second homes, and this could have a devastating effect in areas with higher concentrations of second homes.

The capping of the deduction for state and local property taxes (SALT) at $10,000 will also negatively impact states with high property taxes, such as California, Connecticut, and New York. Furthermore, proposed changes to the capital gains exemption on profits from the sale of a home (requiring five years of continuous residence as compared to the current two) could impact approximately 750,000 home sellers a year and slow the growth of home ownership.

Something else to consider is that all of the aforementioned changes will only affect new home purchases, which I fear might become a deterrent for current home owners to sell. Given the severe shortage of homes for sale in a number of markets across the country, this could serve to exacerbate an already-persistent problem.

Housing Bubble

Housing Bubble

I continue to be concerned about housing affordability. Home prices have been rising across much of the country at unsustainable rates, and although I still contend that we are not in “bubble” territory, it does represent a substantial impediment to the long-term health of the housing market. But if home price growth begins to taper, as I predict it will in 2018, that should provide some relief in many markets where there are concerns about a housing bubble.

In summary, along with slowing home price growth, there should be a modest improvement in the number of homes for sale in 2018, and the total home sales will be higher than 2017. First-time buyers will continue to play a substantial role in the nation’s housing market, but their influence may be limited depending on where the government lands on tax reform.”